Living abroad as a US expat brings a unique set of financial opportunities and challenges. Among these challenges is the obligation to navigate and comply with the United States tax laws, which can be particularly intricate when it involves foreign assets and transactions. The foreign gift tax is a lesser-known but significant aspect of these regulations. For US citizens and residents living overseas, receiving gifts from foreign individuals or entities comes with specific reporting requirements and potential tax implications that must be carefully managed.

The concept of a foreign gift tax is rooted in the US government’s desire to ensure that all income, regardless of its origin, is reported and considered for tax purposes. The IRS has established rules to monitor and regulate the flow of significant gifts from foreign persons to US persons to prevent tax evasion and maintain transparency in financial transactions. These rules are essential for US expats to understand, as failure to comply can result in severe penalties.

If you need assistance with reporting a gift you received, feel free to contact Universal Tax Professionals. Our team of international tax accountants would be delighted to provide insights on how to handle your situation. We also offer a wide range of other US expat tax services to help Americans living abroad.

What is Foreign Gift Tax?

A foreign gift, for US tax purposes, refers to any gift received by a US person from a foreign person. This can include:

- Gifts from non-resident alien individuals: Individuals who are not US citizens or residents.

- Gifts from foreign estates: Estates of deceased individuals who were non-resident aliens at the time of their death.

- Gifts from foreign corporations and partnerships: Entities that are organized and operated outside the United States.

- Gifts from foreign trusts: Trusts that are not considered domestic under US tax law.

These gifts can come in various forms, such as cash, real estate, stocks, or other types of property. The IRS is primarily concerned with tracking these gifts to ensure compliance with tax laws and to prevent tax evasion.

Who needs to file a Gift Tax Return?

A US person must file a gift tax return if they receive:

- More than $100,000 from a non-resident alien individual or foreign estate: If the total value of gifts received from a non-resident alien individual or a foreign estate exceeds $100,000 during the tax year, the recipient must report these gifts to the IRS.

- More than $16,388 from foreign corporations or foreign partnerships: For gifts received from foreign corporations or partnerships, the reporting threshold is significantly lower. If the total value of gifts exceeds $16,388, they must be reported.

It’s important to note that the thresholds apply to the total value of gifts received from each donor category. For example, if you receive multiple gifts from a foreign individual, you must add the value of all gifts to determine if the $100,000 threshold is met.

Do US Expats need to pay Gift Taxes?

In general, the responsibility for paying gift taxes in the United States falls on the donor, not the recipient. This means that if you receive a gift, you are typically not required to pay gift taxes. Instead, the person giving the gift (the donor) is responsible for reporting and potentially paying taxes on the gift if it exceeds certain thresholds.

The US cannot impose its tax laws on foreign donors who do not reside in the United States or do not have US assets. As a result, foreign individuals who give gifts to US persons are not subject to US gift tax laws. Consequently, the recipient (the US expat) is not responsible for paying US gift taxes on these foreign gifts.

While US expats do not pay gift taxes on foreign gifts, they have significant reporting obligations to the IRS. These reporting requirements are designed to ensure transparency and prevent tax evasion. Therefore, the primary concern for US expats is accurate and timely reporting rather than the payment of gift taxes.

Reporting Foreign Gifts

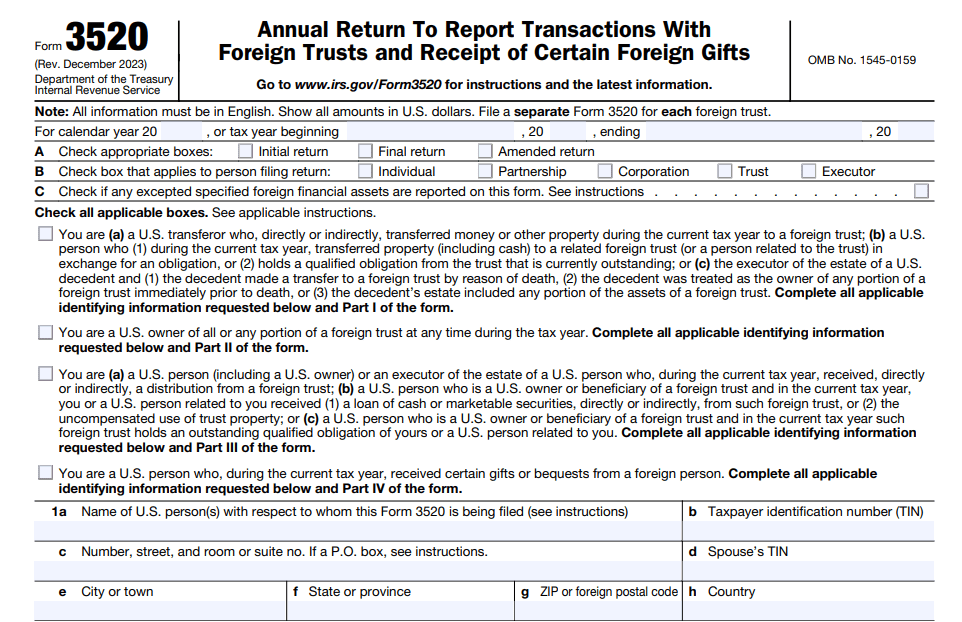

US expats must report foreign gifts to the IRS using Form 3520, Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain Foreign Gifts. This form is used to provide detailed information about the foreign gifts received during the tax year.

Form 3520 requires the following information:

- The name, address, and taxpayer identification number (if available) of the foreign donor.

- The date and amount of each gift received.

- A description of the property received, including its fair market value.

- Trustee name and address

- Any US trust beneficiary personal identifying information such as name, address, and social security number.

- An EIN needs to be included on the form if anything is received from a foreign trust. This can be obtained by filing an SS-4, which is needed for it to be accepted.

- Any relevant information about the relationship between the donor and the recipient.

This form must be filed by the due date of the recipient’s income tax return, including extensions. For most US expats, this means the form is due on April 15, with an automatic extension to June 15 for those living abroad. Additional extensions can be requested until October 15.

Failure to file Form 3520 or providing inaccurate information can result in significant penalties. The IRS imposes a penalty equal to the greater of $10,000 or 5% of the value of the foreign gift for each month the form is late, up to a maximum of 25% of the gift’s value. This means that non-compliance can lead to substantial financial consequences.

Are there any exceptions to the Gift Tax Reporting Requirement?

When it comes to reporting foreign gifts, there are specific exceptions that US expats should be aware of. Understanding these exceptions can help ensure accurate compliance and reduce the reporting burden. Here are some key exceptions to the reporting requirements for foreign gifts:

1. Qualified Tuition or Medical Payments

Payments made on behalf of a US person directly to an educational or medical institution for tuition or medical expenses are not considered gifts and are therefore not subject to the reporting requirements.

For example:

- Tuition: If a foreign relative pays a US person’s tuition directly to the school, this payment is not considered a gift and does not need to be reported.

- Medical Expenses: Similarly, if a foreign individual pays a US person’s medical bills directly to the hospital or medical provider, this payment is excluded from the reporting requirements.

2. Corporate and Partnership Transfers

Transfers that are considered corporate distributions or partnership distributions rather than gifts are not subject to the same reporting requirements. However, these transfers may have other reporting obligations under different tax code sections.

3. Gifts from Foreign Trusts

Gifts received from foreign trusts may be subject to different rules and may not always be classified as reportable gifts. Instead, they might be considered distributions, which have their own set of reporting requirements under Form 3520-A.

4. Small Gifts and Personal Items

Gifts that are small in value or personal items such as birthday presents, holiday gifts, or other occasional gifts of a nominal amount may not trigger the reporting requirements if they are below the specified thresholds.

5. Gift from Spouses

Gifts received from a non-resident alien spouse are not subject to the same reporting requirements. However, normal gift tax rules apply if the spouse is considered a US person.

Navigating the complexities of foreign gift tax regulations as a US expat requires a clear understanding of reporting requirements, exceptions, and compliance obligations. While reporting foreign gifts can seem daunting, especially with varying thresholds and exceptions, informed knowledge and proactive measures can significantly ease the process.

Understanding that most foreign gifts are not subject to taxation for the recipient but require accurate reporting is key. Form 3520 serves as the primary tool for reporting and capturing essential details about the gifts received from non-US sources that exceed specified thresholds. Exceptions such as direct payments for tuition or medical expenses to institutions, gifts below reporting thresholds, and transfers between spouses or US persons are important nuances that can mitigate reporting obligations.

While foreign gift tax regulations add a layer of complexity to expatriate financial management, they also uphold transparency and fairness in cross-border transactions. Embracing these regulations as part of responsible tax compliance ensures that US expats can navigate their international lifestyles with peace of mind, knowing they are meeting their obligations under US tax law.