As cryptocurrency becomes increasingly popular, many Americans are adding digital assets like Bitcoin, Ethereum, and other coins to their portfolios. However, cryptocurrency isn’t just an investment or a currency; it’s also a taxable asset that needs to be reported on your US tax return. The IRS has established clear guidelines on how to report cryptocurrency transactions, but for many, the rules can seem confusing.

If you need assistance with expat tax preparation involving cryptocurrency, contact Universal Tax Professionals. With over a decade of experience in US expat taxes and a deep understanding of international taxation, we are here to help simplify the process for you.

Understanding Cryptocurrency Taxation Basics

In the eyes of the IRS, cryptocurrency is classified as property, not currency. This means that cryptocurrency transactions are subject to the same tax rules that apply to other forms of property, like stocks and real estate. Here’s a quick breakdown:

Capital Gains and Losses: When you sell or exchange cryptocurrency, you may realize a capital gain or loss. If you held the cryptocurrency for over a year before selling, any gain is a long-term capital gain; otherwise, it’s short-term.

Ordinary Income: If you receive cryptocurrency as payment for goods, services, or mining rewards, it is treated as ordinary income.

Cryptocurrency Events Triggering a Taxable Event

Taxable events refer to specific activities that must be reported on your tax return and can potentially result in a tax liability. Here are the primary taxable events involving cryptocurrency:

Selling Cryptocurrency: Selling cryptocurrency for fiat currency (e.g., USD) generates a taxable event. The difference between the selling price and your cost basis (the original purchase price) results in either a capital gain or a loss.

Exchanging Cryptocurrency: Exchanging one cryptocurrency for another (like trading Bitcoin for Ethereum) is also a taxable event. The IRS treats this as if you’ve sold the Bitcoin and purchased Ethereum, meaning you need to calculate the capital gain or loss.

Using Cryptocurrency for Purchases: Using cryptocurrency to buy goods or services triggers a taxable event. The IRS treats this as if you sold the cryptocurrency for cash to make the purchase, so you must report any gain or loss based on the asset’s fair market value on the transaction date.

Receiving Cryptocurrency as Income: Receiving cryptocurrency as compensation, whether as payment for a job, mining rewards, or staking income, is taxable as ordinary income. The value of the cryptocurrency on the date it’s received determines the income amount.

How to Report Cryptocurrency Capital Gains and Losses

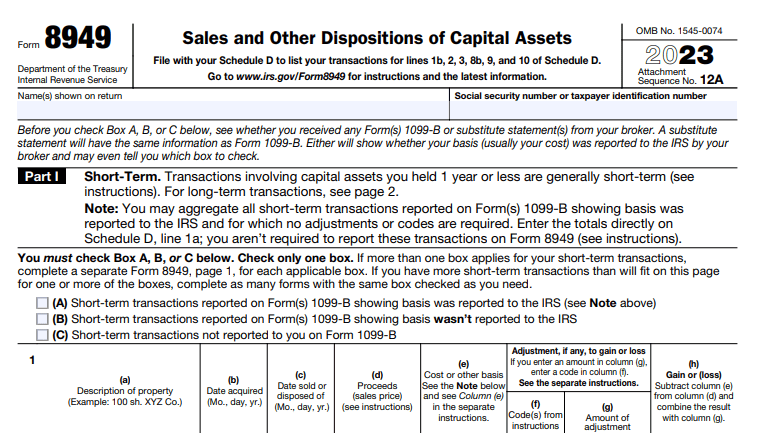

If you have capital gains or losses from cryptocurrency sales, exchanges, or purchases, you’ll need to report them on Form 8949 and Schedule D. Here’s how:

Form 8949: This form details each transaction involving a capital asset. You’ll need to include information like:

- Description of the asset (e.g., “Bitcoin”)

- Date acquired and sold

- Proceeds (selling price or value received)

- Cost basis (purchase price plus any fees)

- Gain or loss from the transaction

Each cryptocurrency transaction should be entered individually on Form 8949.

Schedule D: After completing Form 8949, you transfer the totals for short-term and long-term gains and losses to Schedule D of Form 1040. Schedule D summarizes all capital gains and losses for the tax year, including those from other types of investments like stocks or bonds.

Reporting Cryptocurrency as Income

Cryptocurrency income, whether from mining, staking, airdrops, or payments, must be reported as ordinary income on your tax return. Here’s a look at where and how to report it:

Form 1040: Report any cryptocurrency income as “Other Income” on Schedule 1 of Form 1040. If you earned cryptocurrency through self-employment or freelancing, report it on Schedule C.

Fair Market Value (FMV): When reporting, calculate the fair market value of the cryptocurrency in US dollars on the day it was received. Many exchanges provide historical pricing, which can simplify this step.

Special Circumstances: Forks, Airdrops, and Mining

In some cases, cryptocurrency holders may receive additional assets due to forks, airdrops, or mining activities. Here’s how each is treated for tax purposes:

Hard Forks: If a cryptocurrency undergoes a hard fork, creating a new coin, and you receive the new coin, the IRS treats it as taxable income. You should report the fair market value of the new coin on the day it’s received as income on Schedule 1.

Airdrops: Similar to hard forks, airdrops (free distribution of tokens) are treated as income. You must report the fair market value of any airdropped tokens on the day they’re received.

Mining and Staking: Mining and staking income is subject to ordinary income tax based on the fair market value of the cryptocurrency when it’s earned. If you’re mining as a business, you may also be able to deduct expenses related to mining activities, such as electricity and equipment, on Schedule C.

Keeping Accurate Records for Cryptocurrency Transactions

Cryptocurrency transactions can be numerous and complex, so keeping precise records is critical for accurate tax reporting. Here’s a list of records to maintain:

- Transaction Details: Record the date, type, and amount of each transaction.

- Fair Market Value: Note the USD value of the cryptocurrency at the time of each transaction.

- Cost Basis: Track the amount paid or the fair market value when you acquired the cryptocurrency.

- Fees: Keep records of any transaction fees, as these can be included in your cost basis or subtracted from sale proceeds.

Many taxpayers use cryptocurrency tax software like CoinTracker, Koinly, or TaxBit to help track, calculate, and organize their transactions.

IRS Virtual Currency Question on Form 1040

Since 2020, the IRS has included a specific question about virtual currency on Form 1040, directly asking taxpayers if they received, sold, sent, exchanged, or otherwise acquired any financial interest in cryptocurrency during the tax year. Be honest here, as answering “No” if you’ve engaged in any of these activities could have legal repercussions if later audits reveal cryptocurrency activity.

Tax Planning Tips for Cryptocurrency Holders

To minimize your tax liability and stay compliant, consider these tax planning strategies:

- Use Tax-Loss Harvesting: Sell losing assets to offset gains from profitable transactions, reducing overall capital gains tax.

- Consider Holding Periods: Long-term capital gains (assets held over a year) are taxed at a lower rate than short-term gains. If possible, wait to sell assets until you’ve held them for over a year.

- Track Cost Basis: Use a consistent method to track your cost basis, such as FIFO (first-in, first-out) or LIFO (last-in, first-out), to simplify reporting and potentially lower your tax liability.