If you’re a small business owner considering your company’s structure, the S Corporation (S Corp) is likely to come up as an appealing option. S Corporations offer certain tax benefits and limited liability for their shareholders, making them a popular choice for many entrepreneurs. However, running an S corporation involves specific legal and financial responsibilities, particularly regarding tax compliance.

If you’re seeking expert guidance in establishing an S corporation or comprehending the tax ramifications of forming one, don’t hesitate to contact Universal Tax Professionals. Our team of international tax accountants specializes in navigating the complexities of corporate tax returns and can assist you with your tax and accounting obligations.

What is an S-Corporation?

An S corporation is a business entity that elects a special tax status with the Internal Revenue Service (IRS) under Subchapter S of the Internal Revenue Code (IRC).

An S Corp is a type of corporation that elects to pass corporate income, losses, deductions, and credits to its shareholders for federal tax purposes. This means that the S Corp generally does not pay federal income taxes at the corporate level. Instead, the corporation’s income or losses are “passed through” to the shareholders’ personal tax returns, which are reported and taxed accordingly.

What are the requirements for forming an S Corporation?

To be eligible for an S Corporation status, a business must meet specific criteria set forth by the Internal Revenue Service (IRS). These qualifications are designed to ensure that the business structure aligns with the requirements for pass-through taxation and other characteristics unique to S corporations.

Here are the key qualifications for S-corporation status:

Domestic Corporation: The business must be a domestic corporation incorporated in the United States. Foreign corporations, partnerships, and certain financial institutions are generally ineligible for S Corporation status.

Allowable Shareholders: S corporations are restricted to having no more than 100 shareholders. These shareholders must be individuals, certain trusts, estates, or tax-exempt organizations. Non-resident aliens, corporations, and most partnerships cannot be shareholders in an S corp.

One Class of Stock: An S corporation can only have one class of stock. This means that all corporation shares confer identical rights to distributions and liquidation proceeds. Different voting rights are permissible, but economic rights must be the same.

Eligible Entity Election: The corporation must elect S corporation status by filing Form 2553 with the IRS. This election must typically be made within two and a half months (75 days) of the beginning of the tax year in which the election is to take effect or at any time during the preceding tax year.

Tax Year and Accounting Method: An S corporation must use the calendar year (January 1 to December 31) unless it can establish a business purpose for using a different fiscal year. Also, the corporation generally must use the cash method of accounting.

Qualified Business Activities: Certain businesses are ineligible for S-corporation status, including insurance companies, domestic international sales corporations (DISCs), and certain financial institutions.

S Corporation Tax Forms

There are specific tax forms that an S Corp must file with the Internal Revenue Service (IRS) to report income, deductions, credits, and other relevant financial information.

IRS Form 1120S – US Income Tax Return for an S Corporation

Form 1120S serves as the primary tax return for S corporations. It reports the S corporation’s income, deductions, gains, losses, credits, and other tax-related items to the IRS. The form helps determine the corporation’s taxable income and calculates the amount of tax owed (if any) to the IRS.

Form 1120S calculates and allocates the corporation’s income, losses, deductions, and credits among its shareholders. This allocation is reported to each shareholder through Schedule K-1 (Form 1120S), which outlines their share of the corporation’s financial activities.

Instructions and Components of Form 1120S

Part I: Income

- Gross Receipts or Sales (Line 1a): Report the total gross receipts or sales generated by the S corporation during the tax year. Include all revenue earned from the sale of goods or services.

- Returns and Allowances (Line 2): Deduct any returns or allowances given to customers during the tax year from the gross receipts.

- Cost of Goods Sold (Lines 3-10): Provide details of the cost of goods sold, including opening and closing inventories, purchases, and other costs related to goods sold. Calculate the cost of goods sold using the applicable methods (e.g., FIFO, LIFO).

Part II: Deductions

- Salaries and Wages (Line 7): Report wages and salaries paid to employees of the S corporation. Include all compensation, bonuses, and other payments to employees.

- Rent Expense (Line 8): Enter the total amount of rent paid for business premises or equipment used in the operation of the S corporation.

- Taxes and Licenses (Line 9): Include federal, state, and local taxes paid by the S corporation, such as income taxes, property taxes, and payroll taxes.

- Interest Expense (Line 10): Report interest paid on loans or other forms of borrowed capital used for business purposes.

- Depreciation and Amortization (Lines 13-17): Provide details of depreciation and amortization expenses for assets used in the S corporation’s business. Include information on the method of depreciation (e.g., MACRS) and the useful life of assets.

Part III: Income (Loss) and Other Information

- Other Income (Line 21): Report any additional sources of income not included in gross receipts, such as interest income or dividends.

- Other Deductions (Line 23): Include deductions not captured in other sections of the form, such as bad debts or charitable contributions.

Part IV: Analysis of Net Income (Loss)

- Net Income (Loss) (Line 24): Calculate the net income or loss of the S corporation by subtracting total deductions from total income.

Part V: Shareholder’s Information

- Schedule K-1 (Form 1120S) – Shareholder’s Share of Income, Deductions, Credits, etc.: Provide each shareholder with a Schedule K-1 detailing their share of the S corporation’s income, deductions, credits, and other relevant information. Shareholders use this information to report their portion of S corporation earnings on their personal tax returns.

Other Considerations

Attached Statements and Schedules: Depending on the complexity of the S corporation’s operations, additional statements, schedules, or forms may need to be attached to Form 1120S to provide detailed information. Ensure that any relevant tax elections, disclosures, or adjustments required by the IRS are properly documented and included with the tax return.

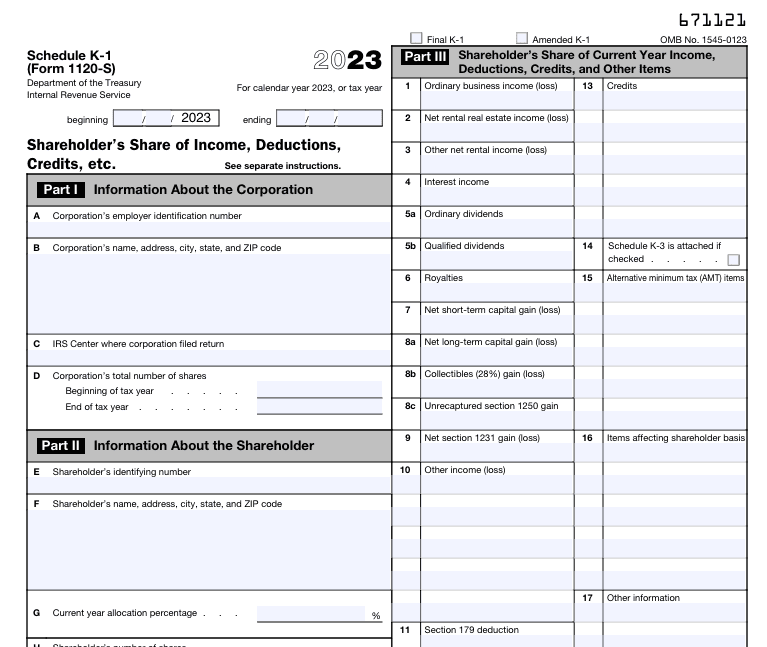

IRS Schedule K-1 (Form 1120S)

Schedule K-1 (Form 1120S) is used by S corporations to provide detailed information to each shareholder regarding their portion of the S corporation’s financial activities for the tax year. The information reported on Schedule K-1 is used by shareholders to report their share of S corporation income or losses on their individual tax returns.

Instructions and Components of Schedule K-1 (Form 1120S)

Part I: Ordinary Income (Loss)

This section reports each shareholder’s share of the S corporation’s ordinary income or loss for the tax year. Components may include business income or loss, rental income or loss, interest and dividend income

Part II: Other Information

This section includes various items that affect the shareholder’s tax liability or basis in the S corporation’s stock. Common items reported in Part II include tax-exempt income, foreign taxes paid, and distributions of cash or property to shareholders.

Part III: Shareholder’s Capital Account Analysis

Schedule K-1 typically includes a capital account analysis, which shows changes in the shareholder’s equity (capital) in the S corporation over the tax year. Components may include beginning and ending balances of the shareholder’s capital account, contributions, and distributions made during the tax year and allocations of income, loss, and other adjustments affecting the shareholder’s capital.

IRS Form 2553 – Election by a Small Business Corporation

Form 2553 is used by qualifying corporations to make an election to be treated as an S corporation for federal income tax purposes.

Key Information Required on Form 2553

When completing Form 2553, the corporation must provide the following information:

- Corporation Information: Legal name, address, Employer Identification Number (EIN), date of incorporation, state of incorporation, and fiscal year-end.

- Effective Date of Election: Specify the tax year in which the S corporation election will take effect.

- Shareholder Information: List the names, addresses, and Taxpayer Identification Numbers (TINs) of all shareholders.

- Consent Statement: Shareholders must sign and date a consent statement affirming their agreement to the S corporation election.

Once Form 2553 is properly completed and filed with the IRS, the corporation will receive an acknowledgment of the S corporation election. The election is typically effective starting from the beginning of the corporation’s tax year, as specified on the form.

2025 S Corporation Tax Deadline and Extension

The tax deadlines and extensions for S corporations are important to understand for compliance with IRS regulations. Here are the deadlines for the key forms related to S corporations:

Form 1120S – US Income Tax Return for an S Corporation

- Tax Deadline: The deadline for filing Form 1120S is generally March 15th every year for calendar year S corporations. For example, for the tax year ending December 31, 2024, the deadline to file Form 1120S would be March 15, 2025. However, since that falls on a Saturday, the deadline for the 2024 tax year is March 17, 2025.

- Extension Deadline: S corporations can request an automatic six-month extension to file Form 1120S by filing Form 7004. For this year, the extended filing deadline for calendar-year S corporations would be September 15, 2025.

Schedule K-1 (Form 1120S) – Shareholder’s Share of Income, Deductions, Credits, etc.

- Tax Deadline for Distributing Schedule K-1: S corporations must provide Schedule K-1 to each shareholder by the original due date of Form 1120S, which is typically March 15th (or the extended deadline if an extension was filed).

- Tax Deadline for Including Schedule K-1 on Individual Tax Returns: Shareholders must use the information from Schedule K-1 to report their share of S corporation income or losses on their individual tax returns, due on April 15, 2025 (or the extended deadline).

Form 2553 – Election by a Small Business Corporation

- Timing of Filing Form 2553: Form 2553 must be filed within specific timeframes to be effective for the desired tax year. Generally, the election must be made no later than the 15th day of the third month of the corporation’s tax year in which the election is to take effect. Alternatively, the election can be made at any time during the preceding tax year to be effective for the current tax year.

Penalties for Late Filing of Form 1120S

The penalties for not filing S corporation (S Corp) forms, such as Form 1120S (US Income Tax Return for an S Corporation) or Form 2553 (Election by a Small Business Corporation), can vary depending on the circumstances and the amount of tax owed.

No Tax Due: If the S Corp return is filed late and no tax is due, the penalty is $235 for each month or part of a month (up to 12 months) if the return is late. This penalty is multiplied by the total number of persons who were shareholders during any part of the corporation’s tax year for which the return is due.

Tax Due: If tax is due and the return is filed late, the penalty is calculated as follows:

- $235 for each month or part of a month the return is late (up to 12 months), multiplied by the total number of shareholders.

- Plus, an additional 5% of the unpaid tax amount for each month or part of a month the return is late, up to a maximum of 25% of the unpaid tax.

For tax returns required to be filed in 2024 that are more than 60 days late, the minimum penalty is the smaller of the tax due, if any, or $485.

Penalties may be waived if the late filing or failure to include required information is due to reasonable cause. However, establishing a reasonable cause can be challenging and requires documentation to support the claim.

S Corporation Advantages and Disadvantages

Operating as an S corporation (S Corp) can offer several advantages and disadvantages compared to other business structures like a C Corporation or LLC.

Here’s an overview of the key pros and cons of an S Corp:

Advantages of S Corporation (S Corp)

Pass-Through Taxation: One of the primary advantages of an S Corp is pass-through taxation. The corporation itself does not pay federal income taxes; instead, income, losses, deductions, and credits are passed through to shareholders’ personal tax returns. This can result in potential tax savings for shareholders.

Avoidance of Double Taxation: S corporations avoid the double taxation that C corporations (C corps) face, where corporate profits are taxed at the entity level and then again when dividends are distributed to shareholders.

Health Insurance Premiums: Shareholders who own more than 2% of an S Corp can deduct their health insurance premiums as an “above-the-line” deduction, reducing their taxable income directly on their personal tax return. This tax benefit allows eligible S Corp shareholders to save on income taxes while still receiving valuable health insurance coverage.

Cash-Basis Accounting: S corps can use cash-basis accounting for tax purposes, which generally simplifies recordkeeping and cash flow management compared to accrual accounting. This means that income and expenses are recorded when cash is received or paid, providing a straightforward method for small businesses to track transactions and report taxable income.

Potential Tax Savings for Reduced Self-Employment Tax: Shareholders actively involved in the business can receive income in two ways: salary or distribution of profits.

- Salary: S Corp shareholders who also perform services for the corporation must pay themselves a reasonable salary for their work. This salary is subject to payroll taxes like any other employee.

- Distributions: Beyond the reasonable salary, shareholders can receive distributions of profits from the corporation, which are not subject to self-employment tax. This can result in tax savings because distributions are not subject to Social Security tax (12.4%) and Medicare tax (2.9%).

Disadvantages of S Corporation (S Corp)

Strict Eligibility Requirements: S corporations have strict eligibility requirements, including limitations on the number and type of shareholders, one class of stock, and U.S. residency requirements for shareholders.

Formalities and Compliance: S corporations must comply with certain formalities, such as holding regular shareholder meetings, maintaining corporate records, and adhering to specific operational and governance requirements.

Complexity in Taxation: While pass-through taxation is a benefit, it can also lead to complexity in tax planning and reporting. Shareholders must carefully track their share of income, losses, deductions, and credits reported on Schedule K-1.

Limited Growth Potential: S corporations may face limitations in raising capital compared to C corporations, as they cannot issue different classes of stock or easily attract venture capital funding.

State-Specific Considerations: S corporation status and taxation rules vary by state, and certain states may impose additional requirements or taxes on S corporations.

10 Common Questions About S Corporation

1. How are S Corporations taxed?

S corporations are pass-through entities, meaning they do not pay federal income tax at the corporate level. Instead, income, losses, deductions, and credits are passed through to shareholders, who report them on their individual tax returns.

2. What is the difference between an S Corporation and a C Corporation?

The main difference is in taxation. S corporations have pass-through taxation, while C corporations are subject to double taxation (taxed at the corporate level and again on dividends). Additionally, S corporations have restrictions on ownership and are limited to one class of stock.

3. Can an LLC be an S Corporation?

No, an LLC (Limited Liability Company) cannot be an S corporation by default. However, LLCs can be taxed as an S corporation by filing Form 2553 with the IRS.

4. What are the advantages of an S corporation over an LLC?

Advantages of an S corporation over an LLC include:

- Lower Self-Employment Taxes: S corporation shareholders can potentially save on self-employment taxes by receiving distributions instead of salary.

- Ease of Transferability: S corporations often have more straightforward transferability of ownership interests compared to LLCs.

No, an LLC (Limited Liability Company) cannot be an S corporation by default. However, LLCs can be taxed as an S corporation by filing Form 2553 with the IRS.

5. What happens if an S Corporation has more than 100 shareholders?

If an S corporation exceeds the 100-shareholder limit or fails to meet other eligibility requirements, it may lose its S corporation status and be treated as a regular C corporation for tax purposes.

6. Do S corporations pay State Taxes?

S corporations are generally pass-through entities for federal tax purposes, meaning they do not pay federal income tax at the corporate level. However, S corporations may be subject to state income taxes depending on the state’s tax laws.

7. Can non-US citizens be shareholders in an S Corporation?

Non-resident aliens cannot be shareholders of an S corporation. Shareholders must be US citizens or residents, certain trusts, estates, or certain tax-exempt organizations.

8. What happens if I want to sell my shares in an S corporation?

Selling shares in an S corporation involves transferring ownership to a new shareholder. The transaction must comply with state laws and the corporation’s bylaws, and the buyer must be an eligible shareholder.

9. Should I dissolve my S corporation if I move abroad?

Moving abroad does not require the dissolution of an S corporation, but it may affect your residency status for tax purposes and require additional tax considerations.

10. Can I receive distributions from my S corporation while living abroad?

Yes, shareholders can receive distributions from an S corporation while living abroad.